3.1. Strengths and Weaknesses

3.1.1. Policies and measures

In terms of solar energy potential, Turkey is advantageous compared to most countries due to its favourable geographical location. Table 2 indicates monthly mean daily global solar radiation and sunshine duration of the country (National Renewable Energy Action Plan 2014).

Table 2

Monthly mean daily global solar radiation and sunshine duration of Turkey

| Months | Global solar radiation [kWh/m2-day] | Sunshine duration [h/day] |

| January | 1.669 | 3.322 |

| February | 2.181 | 3.965 |

| March | 3.117 | 5.322 |

| April | 4.074 | 6.566 |

| May | 4.963 | 8.806 |

| June | 5.625 | 10.833 |

| July | 5.657 | 11.774 |

| August | 5.280 | 11.433 |

| September | 4.109 | 9.333 |

| October | 2.900 | 6.903 |

| November | 2.027 | 5.233 |

| December | 1.512 | 3.322 |

In parallel with the legal regulations regarding electricity generation from solar energy, the total installed solar energy capacity of Turkey reached to 6361 MW by the end of September 2020. the Law No. 5346 on the Utilization of Renewable Energy Resources for the Purpose of Electricity Generation (YEKK), the Law No. 6094 amending the Law No. 5346, the Electricity Market Law No. 6446 (EPK) and the Energy Efficiency Law No. 5627 (EVK) within The Electricity Market License Regulation (EPLY), the Unlicensed Electricity Production Regulation (LEÜY), the Regulation on Domestic Manufacturing of the Parts Used in the Facilities Producing Electricity from RES and the Renewable Energy Resources Area (YEKA) Regulation are the regulations which provide the greatest incentives to the market. By the Law No. 6446 (EPK), the installed capacity of unlicensed solar power plants increased to 6,102.3 MW which is 6.5% of total installed power capacity. The interest in licensed solar energy investments also increased due to the Law No.5346and the Law No.6094 and the total installed power reached a total of 258.9 MW with 25 new plants by the end of September 2020. Besides, the tenders within the scope of YEKA, made significant contributions to renewable energy generation with high domestic production content ratios. The Karapınar YEKA tender which is allocated in Konya-Karapınar for an installed capacity of 1000 MW has an obligation of 60% domestic content ratio. Therefore, a factory with a photovoltaic module production capacity of at least 500 megawatts per year was established to fulfil the obligation (Attachment to the President's Decision 2019, Energy Efficiency Law No. 5627 2007, The Regulation Regarding Unlicensed Power Generation in relation to the Electricity Market 2011, The Regulation on Renewable Energy Resource Areas 2016, YEKA GES-3 2020). However, an obligation demand of a higher domestic content ratio within YEKA tenders was announced by local PV module manufacturers to contribute the development of local PV industry. The manufacturers also demanded incentives for global manufacturers producing PV panel raw materials to establish production facilities in Turkey and sectoral subsidies such as regulations related to customs taxation in raw material purchases and regulations related to VAT in sales in order to be able to compete with imported manufacturers (Market Research for PV Panel Production in Turkey 2020).

Permitting procedures are excessive burdens in Turkish solar energy market slowing down the development of PV systems, especially the ones with small capacity. Bureaucratic delays and insufficient preparation of authorities are the main obstacles which PV system investor faces to carry the process forward. Besides, long grid connection procedures also cause lead times due to the complexity of bureaucratic procedures with too many authorities.

3.1.2. Science and technology

The universities and laboratories which are involved in solar energy research in Turkey are listed in Table 3 (TUBA Solar Technologies Report 2018). These PV-dedicated units are vital for the country to accelerate the increase the PV share in electricity generation. However, the units are too fragmented and neglect cooperation.

Table 3

Solar energy research institutions in Turkey

| Institution | Topics |

| Middle East Technical University, Solar Energy Research and Development Centre (GUNAM) | Crystal silicon, Heterojunction crystal silicon, CdTe thin film, CIGS thin film, Amorphous thin film, DSSC, Perovskite, OPV, CPV, CSP-STE |

| Ege University, Graduate Faculty of Solar Energy | OPV, lamination, system installation |

| Muğla Sıtkı Kocaman University, Clean Energy Resources Research and Development Centre | BIPV, solar car |

| Niğde Ömer Halis Demir University, Nanotechnology Application and Research Center | Heterojunction crystal silicon, Graphene, CZTS thin film, CIGS thin film, Perovskite, Tandem |

| Istanbul Technical University, Energy Institute | OPV |

| TÜBİTAK | Material Institute | OPV, Heterojunction crystal silicon |

| Energy Institute | Inverter technology, li-ion battery |

| National Metrology Institute | PV performance test |

| Anadolu University, Nanoboyut Research Centre | GaAs based multi-junction solar cell |

| Gazi University, Photonics Application and Research Center | DSSC, TiO2 films, Tandem, QWSC |

| Yaşar University, Department of Energy Systems Engineering | BIPV |

Table 4 presents 16 of 22 local PV panel manufacturers filling out the questionnaires provided by Stantec Turkey. 37.5% of the local PV panel manufacturing companies engages in production of solar modules. However, 13% of the companies operate in Engineering, Procurement and Construction (EPC) as well. 19% of the manufacturers are also Independent Power Producers (IPPs). The remaining 31% perform actively in all fields. Table 5 presents the distribution of PV panel and cell production capacities by companies in Table 4 (Market Research for PV Panel Production in Turkey 2020).

Table 4

16 of local PV panel manufacturers in Turkey

| Company trade names | Abbreviated company trade names | Year of establishment | Location | Partnership Structure |

| Alfa Solar Enerji İnşaat Sanayi ve Tic. A.Ş. | Alfa Solar | 2013 | Kırıkkale | 100% Turkish |

| Ankara Solar Enerji İnşaat A.Ş. | Ankara Solar | 2013 | Ankara | 100% Turkish |

| CW Enerji Mühendislik Ticaret ve Sanayi A.Ş. | CW Enerji | 2016 | Antalya | 100% Turkish |

| Elin Elektrik İnşaat Müşavirlik Proje Taahhüt Ticaret ve Sanayi A.Ş. | Elin Enerji | 2017 | Ankara | 100% Turkish |

| Gazioğlu Solar Enerji Sanayi ve Ticaret A.Ş. | Gazioğlu Solar | 2012 | Tekirdağ | 100% Turkish |

| GEST Enerji Sanayi ve Ticaret A.Ş. | Gest Enerji | 2012 | Hatay | 100% Turkish |

| GTC Güneş Sanayi ve Ticaret A.Ş. | GTC | 2013 | Adıyaman | 100% Turkish |

| 2H Enerji ve Yatırım A.Ş. | 2H Enerji | 2018 | Konya | 100% Turkish |

| HT SOLAR Enerji A.Ş. | HT Solar | 2016 | İstanbul | 100% Chinese |

| Mirsolar Enerji Sanayi ve Ticaret A.Ş. | Mirsolar | 2017 | Sakarya | 100% Turkish |

| Ödül Enerji Taahhüt İnşaat Sanayi Ticaret A.Ş. | Ödül Enerji | 2013 | Kayseri | 100% Turkish |

| Parla Solar Hücre ve Panel Üretim A.Ş. | Parla Solar | 2015 | Denizli | 100% Turkish |

| Seha Mühendislik Müşavirlik Ticaret ve Makina Sanayi A.Ş. | Seha Solar | 2016 | Ankara | 100% Turkish |

| Schmid-Pekintaş Güneş Enerji Sistemleri Sanayi ve Ticaret A.Ş. | Schmid-Pekintaş | 2013 | Düzce | Turkish and German |

| Smart Güneş Enerjisi Teknolojileri ArGE Üretim Sanayi ve Ticaret A.Ş. | Smart Solar | 2017 | Kocaeli | 100% Turkish |

| Solarturk Enerji Sanayi Ticaret A.Ş. | Solarturk | 2011 | Gaziantep | 100% Turkish |

Table 5

The distribution of PV panel and cell production capacities by manufacturers presented in Table 4

| Company | PV panel production capacity (MW/year) | PV cell production capacity (MW/year) |

| Alfa Solar | 300 | - |

| Ankara Solar | 200 | - |

| CW Enerji | 1000 | - |

| Elin Enerji | 450 | - |

| Gazioğlu Solar | 140 | - |

| Gest Enerji | 150 | - |

| GTC | 135 | 100 |

| 2H Enerji | 250 | - |

| HT Solar | 800 | 400 |

| Mirsolar | 200 | - |

| Ödül Enerji | 235 | - |

| Parla Solar | 150 | 130 |

| Seha Solar | 100 | - |

| Schmid-Pekintaş | 250 | - |

| Smart Solar | 1000 | - |

| Solar Turk | 250 | - |

Even though PV panel production and PV cell production in Turkey is promising, domestic production capacity of PV panels and PV cells is not sufficient to achieve the sustainable development goal of 10 GW in 2023 (The Eleventh Development Plan (2019-2023)). The primary demand of local manufacturers from policy makers is to prioritise incentives for R&D studies and technological studies related to basic raw material production in renewable energy market policy. The first studies in the field of semiconductor Turkey started in 1983 with the establishment of YITAL Research Centre. IC design, mask production, wafer processing, wafer probing, packaging, circuit test and aging processes are all implemented in YITAL. The semiconductor manufacturing institutions which operate currently are given in Table 6 (Electronic Industry Study Report 2018).

Table 6

The semiconductor manufacturing institutions in Turkey

| Institution | Technology |

| YITAL Research Centre | 250 nm CMOS |

| YITAL Research Centre/ASELSAN | 130 nm CMOS/SiGe |

| YITAL Inc./ASELSAN | 90-65 nm CMOS |

| ODTU-MEMS/ASELSAN | MEMS |

| AB Mikro Nano/ASELSAN | GaN |

| ODTU KANAL, ASELSAN | GaAs, HgCdTe |

| ODTU KANAL, CUNAM, ASELSAN | InGaAs |

| Ermaksan | Fibre Laser |

In the very competitive semiconductor market, incentives by governments are vital for sustainable and developing production in the field. The continuity of incentives in Turkey is vital to provide mass production and meet the local demand in the market, since the production capacities are too small to compete with the foreign markets. The primary demands of the local sector are land supply, tax exemption, discounts on electricity use, discounts on water use, support for employment costs, flexible working law, patents, intellectual property rights, investment support and subsidies (Electronic Industry Study Report 2018).

3.1.3. Market and industry

Turkey reached to 7,219.7 MW installed solar capacity with 7,922 power plants, 7.35% of total installed power capacity. The share of installed solar capacity is 6,572.3 MW by unlicensed plants and 647.4 Mw by licensed plants (TEIAS Installed Capacity Report, June 2021). Within the scope of the Law No. 6446 (EPK), the installed capacity of unlicensed plants was increased to 1 MW which led to a growing interest in unlicensed generation applications in the market. However, the rapid increase in unlicensed generation is not sufficient to meet the 10 GW installed solar capacity objective of the country within 2019-2023 Strategic Plan (The Eleventh Development Plan (2019-2023)).

Mid and long term sustainable development targets of many countries are mostly established presupposing that the local accepts the massive changes in producing and using energy. Several studies from the literature support that solar energy has the highest level of acceptance among the other renewable energy sources (Cranmer et al. 2020, Sütterlin et al. 2017). However, energy-related infrastructure implementations often receive local resistance for several reasons like the size of the plant, the visual and scenic factors, noise annoyance, emotional reactions and safety concerns (Batel et al. 2015, Cousse 2021, Devine-Wright 2019, Huijts et al. 2012). Local acceptance is vital in succeeding sustainable energy development plans, since the opposition from local communities causes delays and raises public concerns. Therefore, policy actors must examine public responses before planning process for sustainability of sustainable energy technologies in the long term. Local prejudice against renewable energy projects is one of the important reasons why Turkey could not experience a higher expansion of renewables given its enormous resource deployment (Kul et al. 2020, Ozgül et al. 2020) .

The Industrial and Technology Strategy established by the Ministry of Industry and Technology announced that one of the primary short-term goals was to support strategic investments in high-tech priority sectors with an end to end mechanism. It is expected to experience a rapid increase in the number of innovative start-ups producing qualified technology integrated with global markets. However, lack of cooperation between industry and research laboratories slow down the process to increase the number and effectiveness of industrial and technology zones. (The Eleventh Development Plan (2019-2023)).

3.2. Opportunities and Threats

3.2.1. Policies and measures

In Turkey, real or legal persons are able to install renewable energy systems up to 5 MW without a license according to the updates introduced with the new Regulation on Unlicensed Electricity Production in Electricity Market (Electricity Market Unlicensed Generation List 2021). There is a growing demand from investors to install unlicensed solar PV energy generation. In 2018, the increase in installed renewable energy generation capacity was recorded 67.35% with 94,47% of solar PV capacity. The target for installed solar capacity by 2023 is reported 10 GW. It However, the ambitious of sustainable development targets of the country in terms of solar PV generation expansion is weak given its geographical favour.

It is a fact that almost all natural gas demand of Turkey, 99%, is met by imports. The country priorities to boost domestic gas exploration and production within energy security strategies. It is announced that the recent Sakarya gas discovery in the Black Sea could promises to greatly diminish the country’s dependence on imported gas. The ambitious of the targets of natural gas security strategies is promising for Turkish economy. However, mid-term long-term clean energy transitions and emission reduction targets must be defined more clearly and ambitiously to achieve sustainable development target in terms of both environment and economy.

Turkey is one of the leading countries for solar water heater systems with a total installed capacity reached to 108,455 [MWth] in 2012 (Benli 2016). However, the great potential of the country can still meet the hot water needs of many more buildings. The key to maximise the potential is to provide government support policies or subsidies for solar water heating applications. Currently, manufacturers benefit from general industry support policies or special projects. On the other hand, there is no incentive for householders to purchase the systems.

PV module manufacturers in Turkey mostly focus on meeting the domestic market demands. Figure 1 shows the production capacity for domestic market and exports. The most important export markets of the companies are Middle East Market with 27.5%, Europe Market with 19.6% and North Africa Market with 15.7% (Market Research for PV Panel Production in Turkey 2020). Nevertheless, the available exporting capacities of local manufacturers are still too small to compete with foreign industry, especially Asian industry.

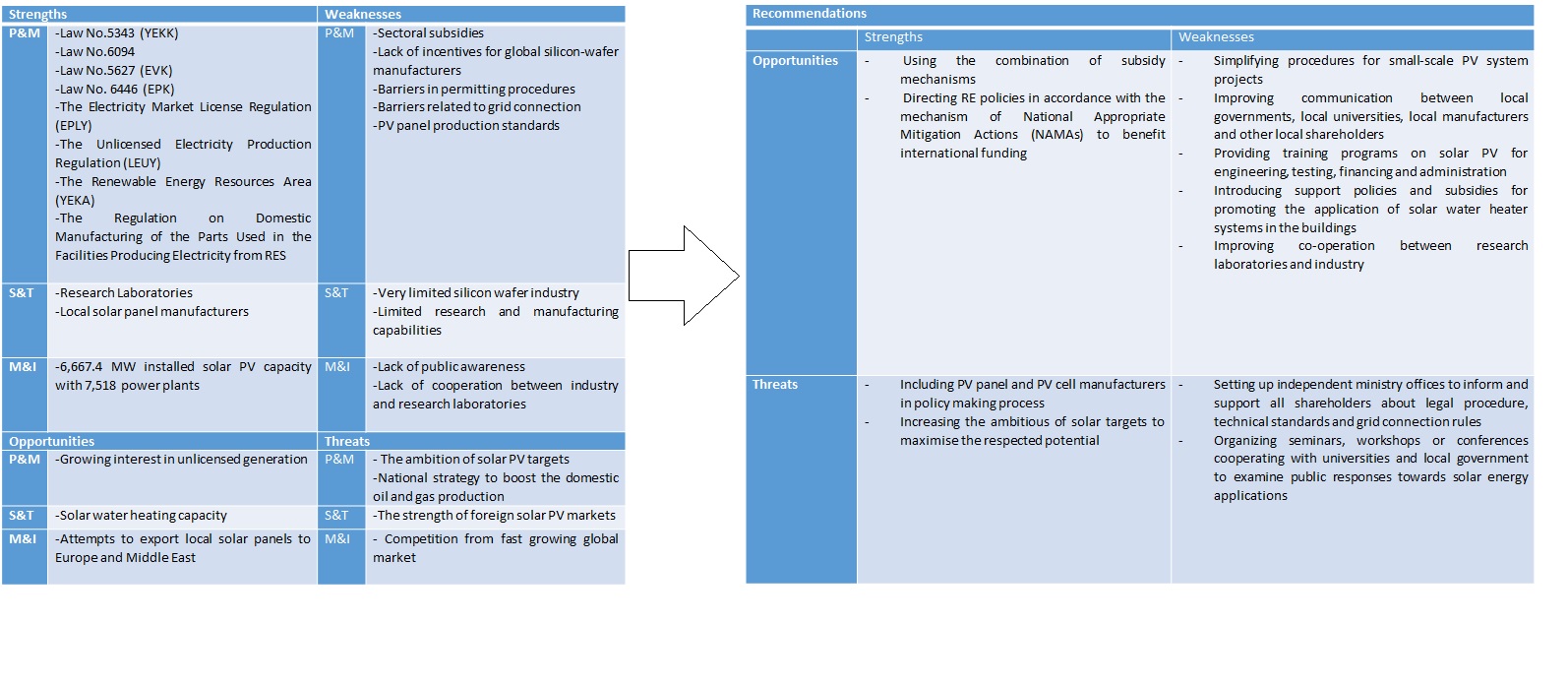

3.3. Recommended strategies

Table 7

Strategies recommended by SWOT analysis presented in Table 1

| | Strengths | Weaknesses |

| Opportunities | - Using the combination of subsidy mechanisms - Directing RE policies in accordance with the mechanism of National Appropriate Mitigation Actions (NAMAs) to benefit international funding | - Simplifying procedures for small-scale PV system projects - Improving communication between local governments, local universities, local manufacturers and other local shareholders - Providing training programs on solar PV for engineering, testing, financing and administration - Introducing support policies and subsidies for promoting the application of solar water heater systems in the buildings - Improving co-operation between research laboratories and industry |

| Threats | - Including PV panel and PV cell manufacturers in policy making process - Increasing the ambitious of solar targets to maximise the respected potential | - Setting up independent ministry offices to inform and support all shareholders about legal procedure, technical standards and grid connection rules - Organizing seminars, workshops or conferences cooperating with universities and local government to examine public responses towards solar energy applications |

3.3.1. Strength and opportunity (SO) strategies

The SO1 strategy focuses on using the combination of subsidy mechanisms to drive more interest across the country with very abundant solar resources far surpassing many market leaders (Global Solar Atlas 2020).

The SO2 strategy focuses on directing RE policies in accordance with the mechanism of National Appropriate Mitigation Actions (NAMAs) to benefit international funding. Since solar energy transition actions promise significant greenhouse gas emission reduction, the government can benefit the instrument to strengthen the national response to climate change (Fridahl et al. 2017).

3.3.2. Weakness and opportunity (WO) strategies

The WO1 strategy focuses on simplifying procedures for small-scale PV system projects. Reducing the number of authorities involved in permitting procedures and defining reasonable deadlines for permitting procedure can remove administrative obstacles that PV system investors tackle.

The WO2 strategy focuses on improving communication between local governments, local universities, local manufacturers and other local shareholders to determine local solar energy transition policies more accurately. Resilient green cities with economies of scale and educated society have a key role to achieve sustainable development goals of governments.

The WO3 strategy focuses on providing training programs on solar PV for engineering, testing, financing and administration to sustain technical, institutional and political improvement on local and national level.

The WO4 strategy focuses on introducing support policies and subsidies for promoting the application of solar water heater systems to minimize the building based greenhouse gas emissions.

The WO5 strategy focuses on improving co-operation between research laboratories and industry to reach a critical mass for national solar energy infrastructure.

3.3.3. Strength and threat (ST) strategies

The ST1 strategy focuses on including PV panel and PV cell manufacturers in policy making process. The sector report indicates that the target of local PV manufacturers is to increase their share in the foreign market aggressively to compete the fast-developing foreign industry. However, additional tariff support, interest rate cut in investment incentives and simpler investment permit processes are requested to achieve the targeted growth in both local and foreign market.

The ST2 strategy focuses on increasing the ambitious of solar targets to maximize the respected potential in all sectors. A more ambitious growth in solar can help the country to achieve the sustainable development goals of domestic energy resource use and emission reduction in energy sector. However, national strategy to boost the domestic oil and gas production may interfere the environmental goals of energy sector.

3.3.4. Weakness and threat (WT) strategies

The WT1 strategy focuses on setting up independent ministry offices to inform and support all shareholders about legal procedure, technical standards and grid connection rules. Clear and consistent guidance in administrative procedures can help to increase the number of solar PV systems accessing to the grid in the short-term.

The WT2 strategy focuses on organizing seminars, workshops or conferences cooperating with universities and local government to examine public responses towards solar energy applications. Addressing all types of responses to solar energy development on policy making can help to achieve the sustainability of solar technologies with a good public acceptance in the long-term.

{kind=link}