Iran government launched the Targeted Subsidy Plan (TSP) in December 2011 to reduce inequality and poverty. In addition, Health Transformation Plan (HTP) was implemented in ministry of health to reduce people out of pocket payment. The study aimed to examine the impact of TSP and HTP on equity in health financing. Relatively significant cash became available for households by introduction of TSP, and as a result, FFC index was improved and the CHE index was reduced. However, over time, the harmful effects of the distribution of money and the growth of liquidity became apparent, and inflation and poverty increased sharply. The TSP increased the inflation rate and as a result restricted the household’s choices and decreased their purchasing power.

Our study found that the FFC index was improved and the CHE index was reduced up to one year after TSP implementation and after then, these indices were deteriorated. Salehi-Isfahani et al. (2015) looking at the impact of TSP three months after its implementation found that TSP reduced inequality and poverty. Similarly, Enami et al. (2019) reported a reduction in inequality and poverty one year after its introduction.

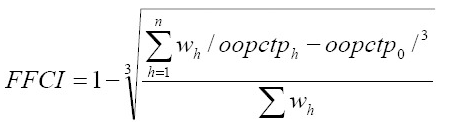

The accurate analysis of the justice index and the survey of households faced with CHE is not possible without identifying target groups and households. Therefore, it is necessary to identify households with a higher probability of Catastrophic Health Expenditure than others, according to their economic and social characteristics as far as possible. The socioeconomic characteristics of CHE households are described in detail in this study.

Considering that people over 65 are considered vulnerable and exposed to high costs of treatment, their presence in households has a positive and significant effect on the bearing catastrophic health expenditures. And as the number of elderly people in households is higher, households are more likely to face CHE. The study by Ma et al (2019), Pal (2012), and Marlis et al (2006), also confirms the result. Some studies have also found it effective for the household to face catastrophic expenditure(Wyszewianski, 1986; Hajizadeh and Nghiem, 2011). This variable was significant and positive in both models at level 99%, which means that an increase in the elderly population in the household increases the probability of suffering from catastrophic health expenditures. The odds of this variable equal 1/59 for the presence of an aged person in the family and 2/21 for the presence more number of aged persons. The household with one elderly and households with 2 elderly and above that, respectively 1.59, 2.21 times more than the non-elderly households exposed to CHE. Due to the aging population in Iran, policymakers should pay particular attention to this issue.

The risk of exposure to catastrophic health expenditures in rural areas is higher urban than areas, which is significant at 99%; rural households are more likely to face catastrophic health expenditures.

As expected, the number of employees in family decreases the chance of suffering from CHE. The negative coefficient and significance level 99% of this variable in the present study confirms this hypothesis, where in households with more number of employees in family, it is more likely for the households to suffer from CHE The odds ratio is equal to 0/70 i.e. households with only a employee and 0/66 i.e. more number of employees. This result is consistent with the studies conducted by (Pal, 2012; Hajizadeh and Nghiem, 2011; Mondal, 2010). One of the innovations of the present study (which is not observed in previous studies) was to consider the development index of the province of the place of residence of households in terms of access to healthcare providers as a factor affecting the probability of facing CHE. According to the results, households living in Iran's less developed provinces have been more exposed to CHE health.

With an increase in the number of educated people in a family, the likelihood of the household exposure to CHE decreases. Given the fact that literacy opportunity is higher in well-off families, and being literate provides more economic opportunities for the individual, literate people are also better off with lifestyles and avoiding high-risk behaviors. As a result, small households are more likely to face CHE. In contrast, Su et al. (2006) showed that the probability of CHE increase by five percent per person added to the household population. The results indicate that households living in mortgage or rental houses more likely suffer from CHE than those who own a home. The coefficient of this variable at the confidence level 99% was significant and negative. The odds ratio is equal to 0.92, and because this ratio is less than one, it is interpreted that property ownership can be a household protecting variable against CHE. Ekman (2007) in his study showed that housing ownership is one of the barrier variables to household CHE healthcare exposure.

Insurance coverage has not reduced the likelihood of household exposure to CHE. This variable was significant at 99% level and its odds ratio was 1.1, Although at the first glance, considering the mechanism of medical insurance (accumulation of risk), health insurance should be a factor in reducing the likelihood of a household to face CHE, and given the rich literature available in this field, including the studies of Samkotra et al(2008). in Thailand, implementation of insurance policies and prepaid mechanisms is considered among the most important factors in protecting households against CHE(Limwattananon et al, 2008). However, limited studies such as the Ekman(2007), WagStaff and Lindlow(2008), Ghiasvand et al (2010), Nekoeimoghadam et al (2013) and O’donnell et al (2008) show that health insurance increases the risk of exposure to CHE for households by encouraging people to use more services as well as more advanced services. And for reasons such as:

-

Inefficiency of health insurance in terms of non-coverage of healthcare services in the sense of not defining suitable packages of services by insurance(Ekman, 2007)

-

Increased induction demand of household and consequently the increased in the share of health expenditure in the household budget(Wagstaff and Lindelow, 2008)

-

The inadequacy of the insurance coverage depth, that is, insurances cover a small share of service expenditure, and the burden of more health expenditure is placed on the shoulder of the household, which increases their risk of facing catastrophic expenditure; the study by Rezapur et al. (2016) conducted in Tehran, confirms the results of the present study(Arab at al, 2016).

Income deciles are a measure of the household's economic situation; the negative and significant effect on these models, at a 99% confidence level, on the probability suffering from CHE, indicates that lower deciles more likely suffer from CHE than households in upper deciles. The results of Sue et al. (2006) and Ekman (2007) also confirm the results of this study.

This result is important in two respects: First, due to the lack of insurance efficiency and the high share of out of pocket payment, lower deciles are more exposed to CHE and second, the prevalence of illness is higher in lower deciles.

Based on the results, granting cash subsidies at a significant level 99% has increased the probability of facing CHE. And because the odds ratio of this variable is more than one, it is construed that subsidies to households cannot be a protective variable for the household against household exposure to catastrophic health expenditures.

A clear picture of the effect of such a plan on the CHE of Iranian households is shown, such that these expenditures have fallen sharply since 2011, and continued in 2012. However, paying cash subsidies directly to bank accounts created a significant leap in the liquidity amount of the people. Based on economic courses, the inflation growth rate is one of the most reliable outcomes of liquidity growth. Although inflation in Iran was 10.13% in 2010, it reached 20.62% in 2011 and reached 27.35% and 39.26% in 2012 and 2013, respectively (based on World Bank data). Of course, inflation has been much worse for the health sector, and health sector inflation exceeded inflation in the entire economy. This situation had a quite devastating effect on the health sector in Iran. The CHE of the households exposed to these costs sharply raised since 2012, and even exceeded the pre-implementation of targeted subsidized. It can be judged that the implementation of this policy has had a negative effect on one of the most important sectors of household welfare, i.e. health.

HTP, a very costly project, has been criticized by many experts. As the budget of the plan is addressed to be 48000 billion Rials, which is believed that its financial burden is out of the power of the government. This plan has been implemented to support households against medical payments, but the changes and effects of other sectors, such as the economy, industry, etc., from which high inflation, increased poverty line, production stagnation, etc. can be named, have weakened the status of lower decile household so that the economic transformation plan has not succeeded even with its primary objective of improving the equity of financing health expenditures. The results of this study indicate that after the implementation of this plan, there has been no change in the status of Iranian households regarding the indices of justice in financing health sector, unless it has prevented the worsening of household health payments.